I remember giving the opening speech at a monetary policy conference in Hong Kong, a.k.a. a junket, featuring Helmut Schleshinger, ex BBK head, Dr. Zeti of Bank Negara and Joseph Yam of the HKMA to polite applause. I used fancy words and convoluted syntax in that wonderful post-modern tradition, glorifying the illustrious speakers while saying virtually nothing. I assumed it was for a good cause.

Throughout the conference very little of substance was debated, the aim of the speakers, it seemed to me, was justifying the practices of their respective governments. Only Mr. Schlesinger, quite a nice, witty fellow and having already retired, threw in a few zingers. Judging solely on what was said at the conference the skies were blue, the global economy was humming and only a fool would complain about then current economic policies.

The date of this little junket in Hong Kong was July, 1997. Yes, July 1997, when the Thai Baht dropped like a stone and the Asian crisis began to shock the investing community and impoverish the working classes in the region. I can even remember getting calls from my office in Singapore during the conference that the Thai Central Bank had been intervening but could no longer stop the Baht from falling. For those of us in the conference, however, such news was the proverbial elephant in the corner.

This memory flashed through my mind while reading Ben Bernanke's, The Benefits of Price Stability. It struck me that I would almost rather prefer to read Dick Cheney speak on The benefits of Hunting Safety than read Bernanke's speech. At least I could laugh at the Cheney irony.

The essence of the speech, in my reading, was that price stability was a worthwhile goal and had been achieved, in contrast to the 70s when, according to Mr. Bernanke, the public's expectations of inflation were not well anchored.

He went on; With little confidence that the Fed would keep inflation low and stable, the public at that time reacted to the oil price increases by anticipating that inflation would rise still further. A destabilizing wage-price spiral ensued as firms and workers competed to "keep up" with inflation.

Think about that statement for a moment.

Is he arguing that after the oil price increases, the public was wrong to expect further price rises? Does he think that once the housing cash machine slows down that current workers won't be pushing for higher wages? Is he arguing that workers' efforts in the 70s to "keep up" with inflation by demanding that wage increases matched price increases were foolish? To whom was the spiral destabilizing? I lived through the period as one of the millions who comprise "the public" and our home was "destabilized" by the oil shock long before wages began to catch up.

Recalling the fetish with GDP measured growth, Bernanke seems to have a fetish with price stability. Not only does he seem to see price stability where there is none, such as within the US economy, he also seems to think it is all good, all the time.

Perhaps Mr. Bernanke should read this report from Robert Gordon, who wonders, Where did the productivity growth go? I guess in Mr. Bernanke's world, that wage gains were accruing disproportionately to the top one percent and 0.1 percent of the income distribution for the past few decades when price stability was the rage is OK.

To the extent the US labor force has been, in fact, as the Fed has trumpeted for years, more productive, should they not have received some of the benefits, either in the form of lower consumer prices or higher wages?

Then again, I really shouldn't be surprised to read such nonsense given the way he opened his speech, praising the efforts of Woodrow Wilson, as I praised the officials in 1997, perhaps with as little thought as, hey, Wilson's from Jersey...I'm from Jersey..

Recognizing that all parties would be served by a central bank that could help contain the periodic financial crises that afflicted the U.S. economy, Wilson worked with the Congress to develop a structure for the central bank that finely balanced competing interests and concerns.

Let's begin at the beginning, Woodrow Wilson didn't work with Congress on either of the two competing bills; the Republican Aldrich Plan, which had only a Central Bank, and the Democratic Federal Reserve Act, which was identical save for having regional banks. Both plans were conceived while Wilson was a little known Governor of New Jersey. The Democratic platform of 1912, Wilson's party, included the Federal Reserve Act.

He goes on:

When the System was founded, its principal legal purpose was to provide "an elastic currency," by which was meant a supply of credit that could fluctuate as needed to meet seasonal and other changes in credit demand. In this regard, the Federal Reserve was an immediate success.

The Federal Reserve was an immediate success in another aspect as well, it centralized the reserves of the nation.

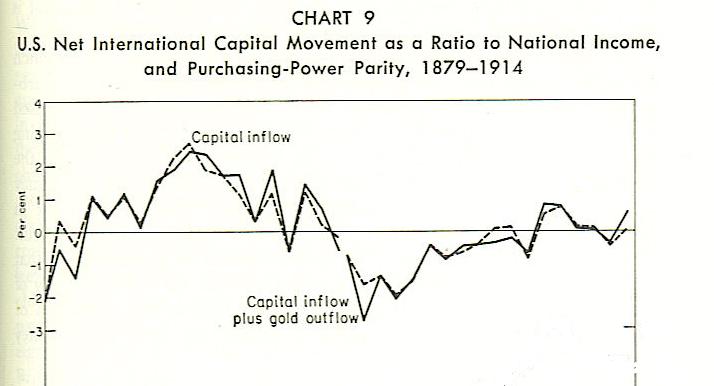

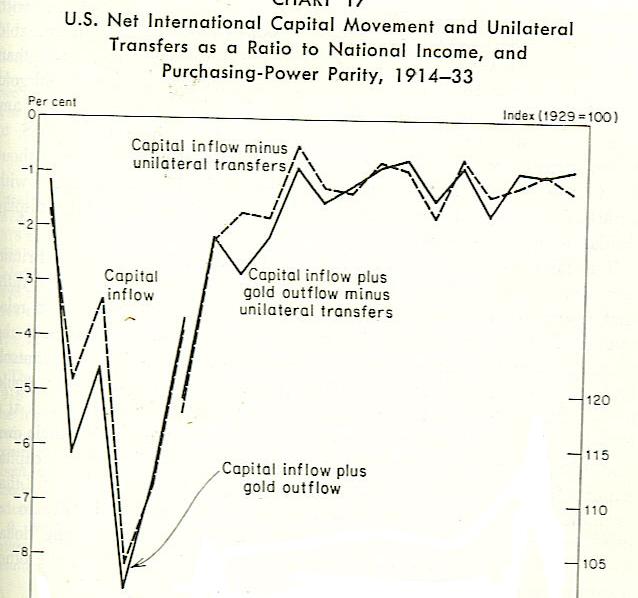

The two graphs below are taken from Milton Friedman's A Monetary History of the United States. Note the capital inflows (positive readings on the graphs) and outflows (negative readings) rarely exceeded 3% of GNP during the period from 1879-1914. Once the Federal Reserve centralized those reserves, they were almost immediately freed to be put to another useful purpose, as demonstrated in the second graph, financing World War I.

If I were Mr. Bernanke, I don't think I would crow so loudly about the achievements of the federal Reserve. Financing two World Wars and since at least 1966, transferring wealth to the top 1% of the nation as if they were doing something wonderful besides indebting future generations and thus creating Buffett's sharecropper society is not something of which I would be proud .

Then again, just as I didn't think much of these things when I was "in the game" I doubt Mr. Bernanke really gives much thought to such details. He's too busy giving speeches and attending meetings to wonder what the real world effects of his price stability fetish or the Federal Reserve in general are. He too likely assumes it is all for a good cause.

0 comments:

Post a Comment