oops, my invite arrived 62 years too late

oops, my invite arrived 62 years too lateWhen I finally arrived at the place I was suitably impressed by the scenery. While much of the world was engulfed in war 62 years ago, hundreds of delegates from around the world met at this wonderful place to devise a new monetary system, with one aim of avoiding some of the causes of the then current war. Jung might have argued that the scenery evoked notions of Olympians looking down on the rest of the world planning the path ahead and in the bright sun light of my first visit, I wouldn't disagree.

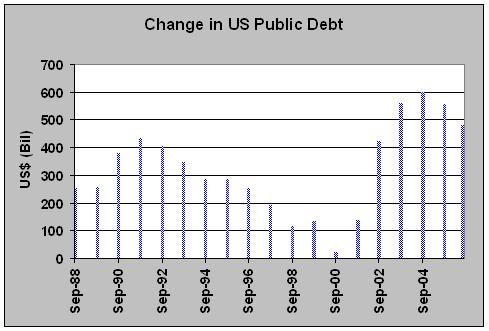

Although much of the world's finances still flow through its remains, the essential elements of the system put in place by these delegates has long since been abandoned. Just as the financiers of the world removed the domestic check and balance of the classical gold standard, which gave the citizenry the right to withdraw real money (specie) from any bank to which they had lent, so too have they removed the international check and balance of the gold exchange standard, which gave sovereign nations the right to withdraw real money (specie) from any national banking system to which they had lent.

With the notion of the removal of the check and balance of specie redemption in mind, consider the recent exchange between William Greider, of Secrets of the Temple fame and Robert, strong $, Rubin.

In response to a question from Greider about rising external imbalances Rubin argues:

Rubin: But I don't think people thought--I'll speak for myself--I surely never thought, if you have the kinds of imbalances you have today, you'd have the kinds of exchange rates we have today, that exchange rates would have substantial adjustments. To put it differently, I never thought in the face of very substantial trade imbalances, you would have inflexible exchange rates. I don't think that was part of anybody's anticipation.

Greider: Does that suggest something else should have happened in the design running up to the current situation?

Rubin: I don't think that's a design issue. I don't think that's actually a trade issue. I think it's a foreign exchange issue.... If you had had fully flexible exchange rates. Though I'm not advocating, by the way, that China go to that immediately because I think it might create a lot of chaos.... But I don't think it's anything in the design in the system. Maybe I'm missing something, but I don't think there's anything in the design of the system we would have done differently....

"So," your author mused to himself while admiring the view at Bretton Woods, "even though the lack of FX adjustment in the face of rising imbalances is a surprise to Rubin, he doesn't think this suggests a design flaw."

Yet, 62 years ago, when the then economic solons of the world designed the system whose remains we currently use, they foresaw the need to have a check and balance to forestall the growth of just such imbalances, in the form of gold redemption. Having removed that check and balance, by changing the system's design, the imbalances, surprisingly to some, grow unchecked and it isn't a design flaw?

On my Bretton Woods trip I began to wonder if the view of humanity that informed the crafters of the system 62 years ago or more to my liking, the view of humanity that informed the founders of this country more than 2 centuries ago, was just that, a trip, a delusion.

Expanding my scope I begin to wonder if it was all just a trip.

Is the US Constitution just a piece of paper? Can unchecked finance produce better results than a regulated (and the rule of specie is one such regulation) system? Should humanity try to adhere to the Geneva Conventions? Is coercion a better method than persuasion coupled with patience while "the penny drops" as the Brits put it? Are systems of morality just the means by which the elite milk their charges?

Or is there something to it? Are there better and worse ways to maintain and further civilization? Civilization, after all, is the goal we seek, not wealth or power which does not exist outside of that context.

I, for one, don't believe it was all just a trip. I believe in the virtue of checks and balances. Power unchecked runs amok, as we see today in many aspects of human relations.

The United States has, correctly in my view, been called an experiment in self-government. Hopefully the experiment can continue before the civilization train leaves the station.